On April 16, at the AICE 2025 SMM (20th) Aluminum Industry Conference and Aluminum Industry Expo—Alumina and Aluminum Raw Materials Forum, co-hosted by SMM Information & Technology Co., Ltd., SMM Metal Trading Center, and Shandong Aisi Information Technology Co., Ltd., and co-organized by Zhongyifeng Jinyi (Suzhou) Technology Co., Ltd. and Lezhi Qianrun Investment Service Co., Ltd., Liu Huimin, Senior Analyst of Aluminum Auxiliary Materials at SMM, shared the current supply and demand situation and price forecast of the Chinese petroleum coke market.

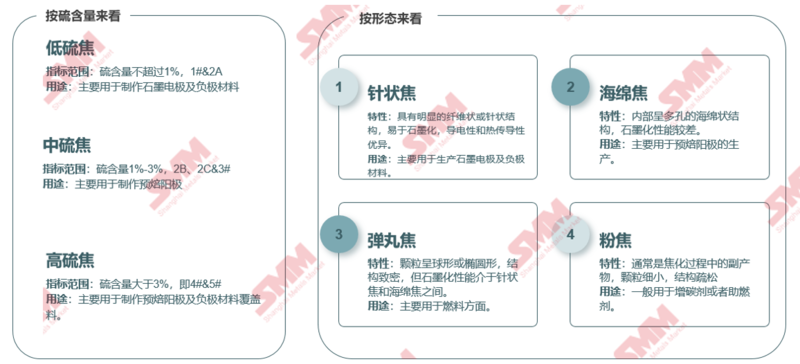

**Petroleum Coke Index Classification Standards**

She elaborated on the NB-SH-T 0527-2019 standard of the petrochemical industry of the People's Republic of China.

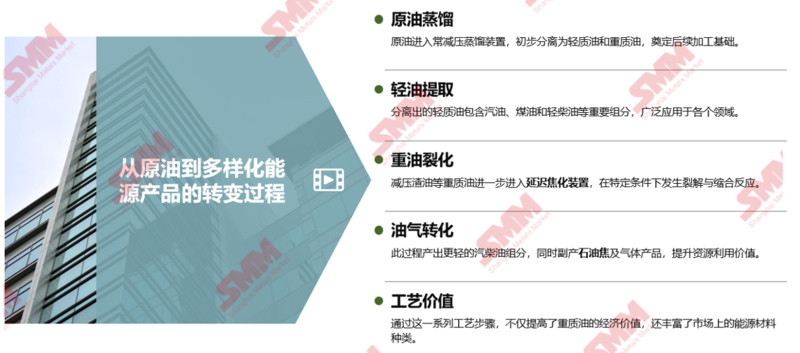

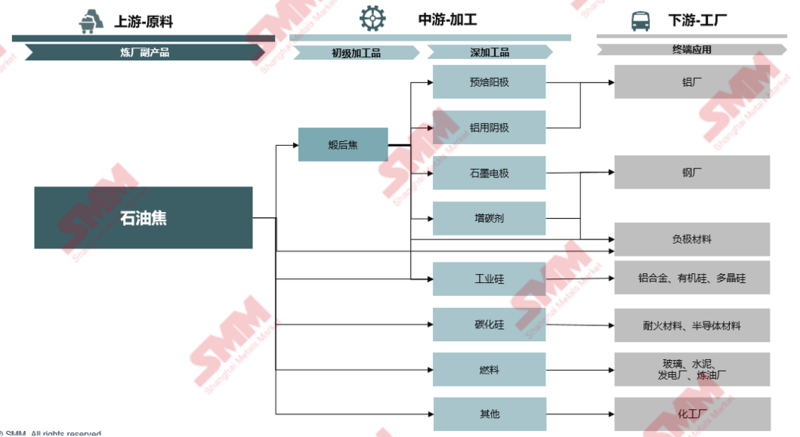

**Where Does Petroleum Coke Come from in the Crude Oil Processing Process?**

**Classification and Uses of Petroleum Coke**

**Supply Landscape of the Chinese Petroleum Coke Market**

Domestic delayed coking unit capacity has increased year by year, with the growth rate significantly slowing after 2023.

**SMM Analysis:**

- From 2020 to 2024, the compound annual growth rate (CAGR) of China's delayed coking unit capacity was approximately 2.6%, with the growth rate reaching 7.15% in 2022, the highest in five years, mainly due to the commissioning of a 6 million mt/year unit by mainstream refineries in 2022.

- As of 2024, China's refinery delayed coking unit capacity was approximately 151 million mt/year, up 1.28% YoY, continuing the growth trend. Among them, the delayed coking capacity of mainstream refineries remained stable, while two enterprises in Shandong added 1.9 million mt/year of capacity, bringing the total delayed coking capacity of local refineries to 71 million mt/year, accounting for 47% of the total capacity. As of now, there is no additional capacity elimination in 2025, and refinery delayed coking unit capacity is transitioning smoothly.

- In recent years, China's total delayed coking unit capacity has maintained an expansion trend. The continuous development of downstream petroleum coke enterprises and increasing domestic demand have laid a solid foundation for the expansion of refinery delayed coking capacity. Additionally, the extended life cycle of delayed coking units and delayed exit steps have maintained the growth trend of domestic petroleum coke supply.

**Distribution of China's Petroleum Coke Delayed Coking Unit Capacity**

**SMM Analysis:**

- By region: East China, South China, Northeast China, and Northwest China rank in the top four. East China and South China are close to coastal ports, facilitating the loading and unloading of crude oil tankers and efficient, low-cost transportation of overseas crude oil, providing stable and sufficient raw materials for delayed coking units. Northeast China and Northwest China are important domestic crude oil production areas, allowing for local sourcing and short-distance transportation of crude oil to refineries, significantly reducing transportation costs and risks, and strongly promoting the growth of local delayed coking unit capacity.

- By province: Shandong ranks first with a total delayed coking capacity of 55.09 million mt/year, accounting for 36% of the total capacity, with concentrated capacity distribution in Dongying, Zibo, and Binzhou.

**SMM Analysis:**

- By group: Local refineries rank first with a total delayed coking unit capacity of 71 million mt/year, accounting for 47%; Sinopec ranks second with a total capacity of 46.75 million mt/year, accounting for 31%; PetroChina ranks third with a total capacity of 24.5 million mt/year, accounting for 16%; CNOOC ranks last with a total capacity of 8.8 million mt/year, accounting for 6%.

- The delayed coking unit capacity of local refineries is mainly distributed in Shandong, Liaoning, and Zhejiang. Especially in Shandong, its capacity accounts for 65% of local refineries. The large number of local refining enterprises, significant industrial cluster effects, proximity to crude oil import ports and domestic crude oil production areas, convenient raw material acquisition, low transportation costs, and complete industrial support.

**China's Petroleum Coke Supply is Mainly High-Sulfur Coke, with No. 4 Coke Accounting for 57%**

**SMM Analysis:**

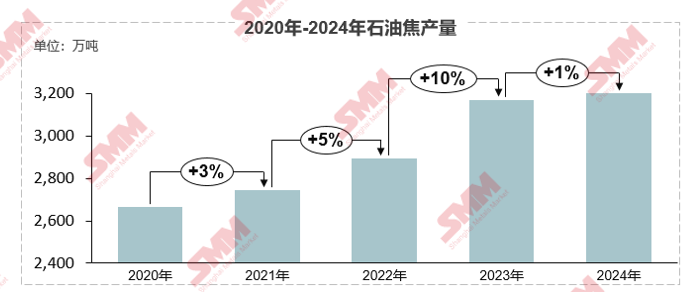

- In 2024, China's petroleum coke production increased to over 32 million mt, up about 1% YoY. China's petroleum coke supply is mainly high-sulfur coke, with No. 4 coke accounting for 57%, followed by medium-sulfur coke accounting for 28%, and low-sulfur coke accounting for only 7%.

- Local refineries account for 73% of high-sulfur petroleum coke production, with No. 4 and No. 5 coke accounting for 68% and 5%, respectively, and medium-sulfur coke No. 2 and No. 3 accounting for 3% and 20%, respectively, with No. 1 accounting for only 4%. High and medium-sulfur coke still dominate, while low-sulfur coke is relatively scarce.

**Total Petroleum Coke Imports Turned Downward in 2024, with High Port Inventory Rapidly Declining**

**SMM Analysis:**

- Since 2019, China's petroleum coke imports have surged, jumping from 8.05 million mt in 2019 to 16.02 million mt in 2023, achieving a doubling growth, with an increase of 99% during the period. The large amount of petroleum coke imports provided sufficient supply for port inventory. From the perspective of petroleum coke port inventory changes in Shandong, port inventory increased significantly in H1 2023, with an increase of 108%, closely related to the continuous increase in imports. A large amount of imported petroleum coke flooded into ports, pushing up inventory levels.

- In 2024, due to the persistently high domestic port petroleum coke inventory, traders' buying sentiment for LME cargoes was moderate, and petroleum coke imports significantly tightened, with total imports of 13.4 million mt, down 16% YoY. With the decline in imports, port inventory continued to destock, with Shandong's petroleum coke port inventory falling 41% to around 1.93 million mt in 2024.

- After entering 2025, Shandong's port petroleum coke inventory fluctuated slightly around 2 million mt.

**US Coke Imports Remained at the Top in 2024, with High-Sulfur Coke Dominating Imports**

**SMM Analysis:**

- In 2024, China's petroleum coke import market showed distinct characteristics, with the US playing a key role. By import source, the US accounted for 3.8614 million mt, representing 28.82% of total imports. Russia ranked second with an import share of 18%, demonstrating its strong strength in the petroleum coke export field. Saudi Arabia accounted for 12%, Canada for 7%, and Colombia and Venezuela each accounted for 6%, collectively forming important suppliers of China's petroleum coke imports.

- By import variety, high-sulfur coke dominated throughout the year. Data from 2024 shows that high-sulfur coke accounted for 71%, medium-sulfur coke for 19%, and low-sulfur coke for 10%. Compared with 2023, the share of high-sulfur coke slightly decreased but still dominated. The share of medium-sulfur coke increased from 14% to 19%, while the share of low-sulfur coke decreased from 12% to 10%.

**US Coke Import Tariffs Escalated, Rising Costs Expected to Lead to a Significant Decline in US Coke Imports**

**SMM Analysis:**

- Since April 2025, the US-China trade friction has intensified, and China has adjusted tariffs on US-origin imported goods multiple times. As of April 11, China's tariffs on US-origin imported goods increased from the initial 34% to 125%, with the effective tariff rate rising to 128%.

- Goods shipped from the place of shipment before 12:01 on April 10 and imported between 12:01 on April 10 and 24:00 on May 13, 2025, are not subject to the additional tariffs.

- As the world's largest petroleum coke producer, the US has a competitive edge in the Chinese market due to its stable supply capability and reasonable pricing system. Based on the current landed price, the cost of US petroleum coke has increased by at least 1,100 yuan/mt, a rise of over 20%, significantly reducing the cost-effectiveness of US petroleum coke imports to China. SMM expects US coke imports to decrease by more than 30%.

**Multiple Factors Intertwined in 2025, Refinery Operating Cost Dilemma Intensified**

**Raw Material Price Increases and Increased Maintenance Enterprises, Domestic Petroleum Coke Supply Reduced in 2025**

**SMM Analysis:**

- Against the above background, since Q1 2025, the frequency of maintenance of domestic refinery delayed coking units has significantly increased. According to SMM statistics, as of the end of March, 32 sets of refinery delayed coking units in China were under maintenance, up about 78% YoY, involving a capacity of 35.9 million mt, up 69% YoY.

- Looking ahead to the full year, it is expected that 20 more sets of refinery delayed coking units will undergo maintenance, involving a capacity of about 28.8 million mt. Based on the refinery maintenance information available so far, mainstream refineries dominate the shutdown units in 2025, accounting for about 70% of the involved capacity. Local refineries have the largest maintenance scale for the year, reaching 34 million mt. The maintenance indicators are mainly high-sulfur coke, with No. 4 petroleum coke accounting for the largest share, reaching 54% of the total capacity.

**Demand Landscape of the Chinese Petroleum Coke Market**

**Overview of Downstream Demand for Petroleum Coke**

**Prebaked Anode: Capacity Increasing Year by Year, Local Supply-Demand Imbalance Evident**

It analyzed the capacity growth of the prebaked anode industry, monthly production of prebaked anodes, monthly production of aluminum enterprises, and the matching of prebaked anode and aluminum capacity.

**Prebaked Anode: Future Capacity Expansion Closely Follows Downstream Demand, Southwest and Mongolia Become Industry Focus Areas**

**SMM Analysis:**

- From 2025 to 2028, a total of 6.17 million mt of prebaked anode capacity is planned to be commissioned. Excluding new plans without indicators, the net increase in domestic aluminum capacity in 2025 and beyond is 650,000 mt. The speed of prebaked anode capacity expansion far exceeds the growth of market demand, exacerbating the surplus problem, and industry competition will become more intense.

- By region of new capacity: Southwest China: Capacity expansion is significant, being the main growth area. New projects in Guangxi, Yunnan, and other places are numerous, attracting aluminum capacity transfer due to abundant hydropower resources, driving prebaked anode demand. Shandong: As the main production area, it continues to expand capacity with raw material and geographical advantages. Inner Mongolia: Due to the transfer of aluminum capacity from Henan and other places, local enterprises have increased production, driving prebaked anode capacity growth.

**Since 2022, Negative Electrode Material Capacity Has Rapidly Expanded, with Effective Capacity Utilization Rate Decreasing Year by Year**

**SMM Analysis:**

- Since 2022, negative electrode material capacity has rapidly expanded, reaching about 4.97 million mt by 2024, with a capacity growth rate of 150%. However, the capacity growth rate far exceeds downstream demand, leading to a supply-demand imbalance and increasingly fierce competition. New capacity is difficult to release, and the effective capacity utilization rate has dropped from 71% to 37%.

- Production in 2022 was 1.41 million mt, and in 2024, it reached 1.84 million mt, with a capacity growth rate of about 31%. Although there is growth, the magnitude is relatively limited compared to capacity expansion, and the production growth trend has been relatively flat over the three years.

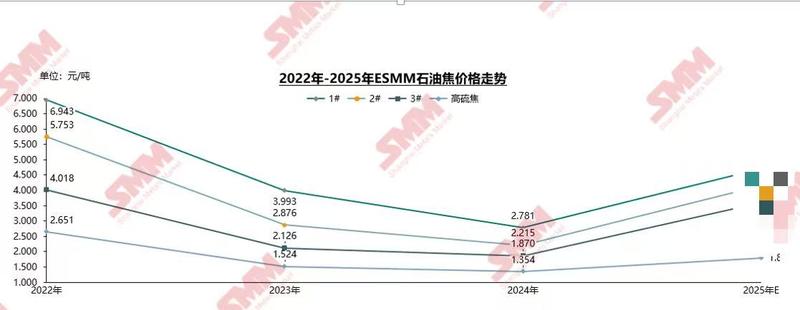

**2024 Petroleum Coke Price Review**

**From September 2024, Low-Sulfur Coke Prices Continued to Rise Supported by Increased Stockpiling Demand**

**SMM Analysis:**

- From January to April 2024, low-sulfur petroleum coke in Northeast China showed an upward trend due to the resumption of the negative electrode material market and increased production schedules of downstream battery factories, leading to rising demand. However, after entering Q2, the execution of downstream orders and the number of new orders of negative electrode enterprises decreased, gradually weakening the demand for petroleum coke procurement. Coupled with the domestic supply surplus, low-sulfur petroleum coke prices began to enter a slight downward fluctuation.

- Starting from the end of Q3 2024, due to the good performance of downstream orders of negative electrode material enterprises, their petroleum coke inventory had dropped to a low level, triggering active stockpiling and restocking. This factor, combined with others, prompted low-sulfur coke prices to turn from decline to rise. Especially in Q1 2025, the concentrated stockpiling during the Chinese New Year holiday and policy interference amplified market expectations, driving a rapid rise in low-sulfur coke prices.

In 2024, the prices of medium and high-sulphur petroleum coke mainly fluctuated, and after entering 2025, the coke prices rose rapidly.

SMM analysis:

ØIn 2024, the prices of medium and high-sulphur petroleum coke in Shandong fluctuated slightly. In Q1, the anode market improved, transactions were active, downstream carbon enterprises were actively purchasing, and prices rose slightly. In Q2, refinery maintenance increased, supply decreased, just-in-time procurement supported prices to rise slightly, and then due to the cooling of procurement sentiment, prices showed a downward trend. In September, local refineries' poor profitability led to an increase in product sulfur content, some enterprises stopped for maintenance, and the supply of medium-sulphur petroleum coke was tight, and prices turned strong. High-sulphur petroleum coke prices rose slightly in Q1 driven by market sentiment, and then fluctuated downward.

ØAfter entering 2025, due to the increase in raw material costs of refineries, some refineries, especially those in Shandong, reduced production, coupled with the Chinese New Year holiday, downstream prebaked anode enterprises concentrated on stockpiling, and petroleum coke prices ushered in explosive growth. The prices of calcined petroleum coke and prebaked anode also rose rapidly with the rise in raw material petroleum coke prices. As of April, the procurement price of prebaked anode of benchmark enterprises rose to 5,205 yuan/mt, an increase of 29% compared with the beginning of the year.

2025 Petroleum Coke Price Forecast

2025 Price Influencing Factors

►Macro and Policy Aspects

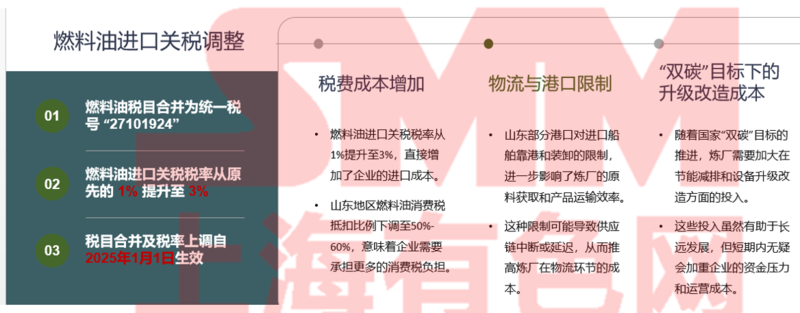

1. Import Tariff Adjustment

From January 2025, the import tariff rate of fuel oil will be increased from the original 1% to 3%, and the fuel oil consumption tax deduction ratio in Shandong will also be significantly reduced from full deduction to the range of 50-60%. From April 12, 2025, a 125% tariff will be imposed on all imported goods originating from the US, and the import tariff will be increased from 3% to 128%.

2. Energy Saving and Carbon Reduction Policy

The "dual carbon" target promotes environmental protection upgrades and tax standardization, and the environmental protection and compliance requirements of local refineries are improved. Shandong Province plans to reduce the crude oil processing capacity of the local refining industry from 130 million mt/year to around 90 million mt/year by 2025, a reduction of 30%, and eliminate backward capacity through integration and other means. In 2024, multiple national departments required the elimination of atmospheric and vacuum units of 2 million mt/year and below, and more than 20% of such units in Shandong were affected.

►Fundamentals

3. Domestic Petroleum Coke Supply

In 2025, there is no plan to add new delayed coking units in China, and the shutdown and maintenance of delayed coking units in refineries are frequent during the year. The loss of maintenance in April-May has increased significantly, coupled with the impact of consumption tax on profit margins, the capacity utilization rate of delayed coking has declined. Based on the above information, the domestic petroleum coke supply is expected to decline in 2025.

4. Petroleum Coke Import Situation

The US is the largest source of petroleum coke imports in China. The import tariff of US coke has been increased layer by layer, and the cost has increased seriously. The total import of US petroleum coke is expected to decrease by 30%-40%. Overall, the import of petroleum coke in 2025 is expected to increase YoY, but the increase is limited, and the tight supply pattern of petroleum coke is difficult to change.

5. Domestic Petroleum Coke Demand

The demand of the aluminum industry is steadily increasing, providing stable support for petroleum coke demand. The demand of emerging new energy fields such as anode materials and PV polysilicon is growing rapidly, becoming an important force to boost petroleum coke demand. However, the demand of some traditional industries, such as the glass industry, is shrinking, and the demand of the silicon metal industry is mediocre. The market demand structure of petroleum coke is continuously reshaping, and the proportion of new energy-related fields is increasing.

Macro fundamentals are favorable for the rise of petroleum coke prices, and the price center of petroleum coke in 2025 will obviously move upward.

SMM analysis:

ØOverall, in the short term, the tight supply and demand situation of petroleum coke is difficult to alleviate, and the probability of price increase is high. From April, the expectation of import contraction has strengthened, coupled with the domestic refineries entering the concentrated maintenance period, and the price has shown an upward trend. In the medium and long term, the new capacity of domestic petroleum coke is less and the expectation of local refinery capacity withdrawal, the supply-demand imbalance has intensified, the dependence on imports has continued to increase, and import obstruction or cost increase will significantly increase the price of petroleum coke.

ØHowever, the price trend also faces some uncertain factors, such as if the macroeconomic situation recovers slowly, the recovery time of the consumption demand of physical enterprises and industrial terminals will be longer, which may inhibit the price increase; if the coal market and related policies change, it will also have an indirect impact on the price of petroleum coke.

》Click to view the special report of AICE 2025 SMM (20th) Aluminum Industry Conference and Aluminum Industry Expo